[ad_1]

small

Regardless of weak administration commentary, Goldman Sachs has maintained its purchase ranking on the inventory with a worth goal of Rs 1,100.

purchase Promote Godrej Client share

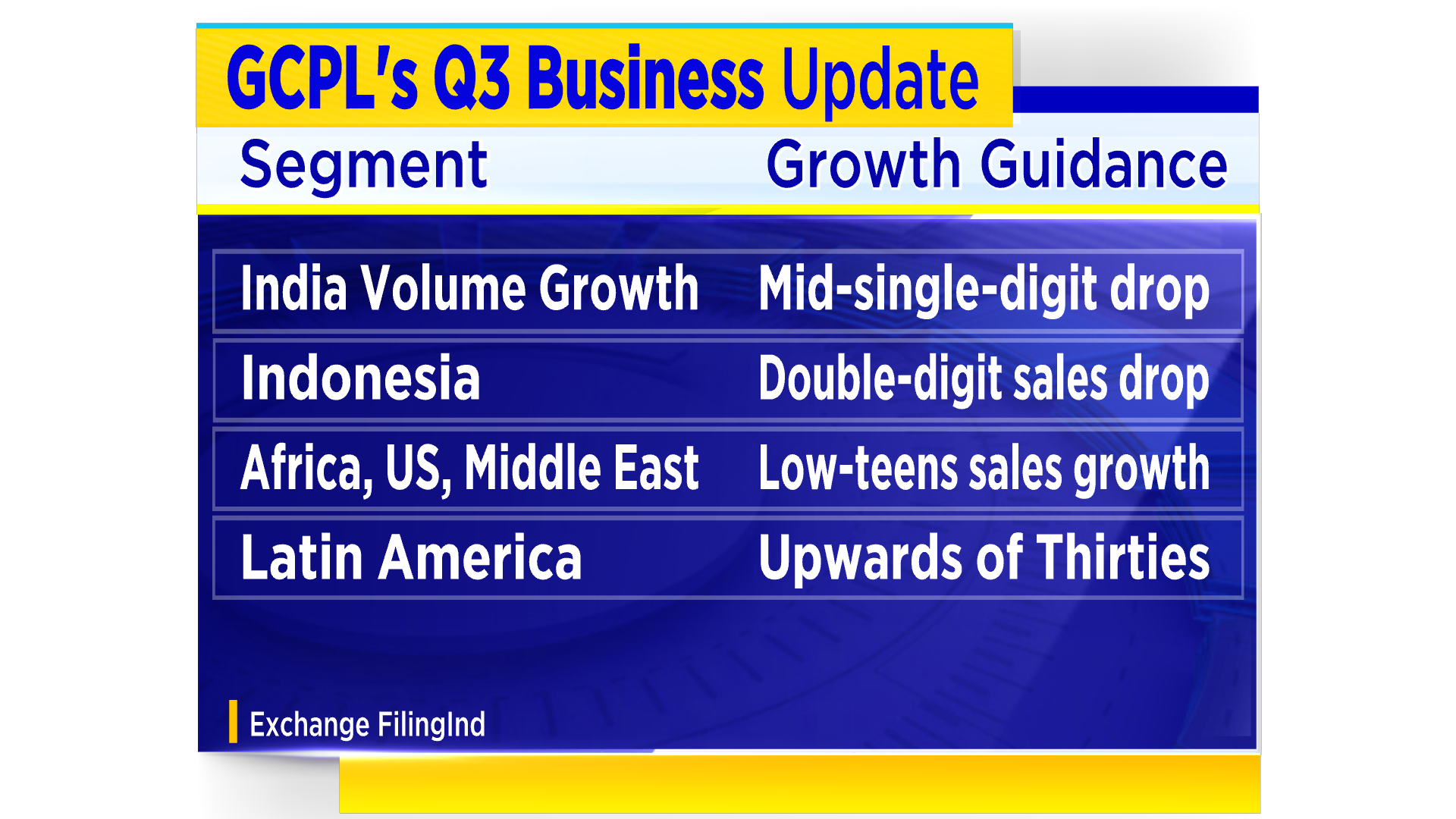

Godrej Client Merchandise Ltd., one of many main gamers in family, air care and aircare merchandise in rising markets, expects India’s enterprise quantity to fall within the mid-single digits within the September quarter, observing a “mushy pattern” within the home FMCG trade. Is.

The India enterprise contributes about 60 % of the corporate’s whole revenue and greater than 80 % of the corporate’s earnings earlier than curiosity, taxes, depreciation and amortization (EBITDA). Consequently, the corporate expects a mid-teens decline in its working revenue. It cited high-cost materials consumption, important upfront advertising and marketing investments to drive the class’s development, and weak efficiency in Indonesia as the explanations behind the warning.

Indonesia is GCPL’s second largest particular person market by nation, excluding the Africa area. The corporate expects the Indonesia enterprise to report a double-digit gross sales decline in fixed foreign money phrases attributable to a discount in demand for hygiene merchandise post-Covid-19.

Nonetheless, on the gross sales entrance, the corporate expects high-single-digit gross sales development for the quarter, led by the non-public care and residential care enterprise. It additionally expects continued present gross sales development for its Latin America enterprise into the excessive thirties.

The corporate can be assured of bettering consumption and increasing gross margins attributable to important restoration in commodities like palm oil derivatives and crude. It expects gross sales development in each Indonesia (excluding sanitation), in addition to its GAUM (Godrej Africa, Center East, USA) enterprise.

Regardless of weak remarks from administration, Goldman Sachs sees Godrej Client as a robust turnaround candidate as development in India’s homecare enterprise improves. The agency can be seeing early indicators of restoration in Indonesia’s enterprise. It expects decrease enter prices to help margins and continued double-digit development within the Africa enterprise because of the firm’s distribution initiatives.

Shares of Godrej Client have misplaced 7 per cent this yr and have misplaced over 20 per cent from 52-week highs.

[ad_2]

Supply hyperlink